Interest Rate Cap Floor And Collar

An Introduction To Caps Floors Collars Swaps And Swaptions Lancaster Pollard

How Interest Rate Collars Work Finance Train

Rate Cap Swap And Collar A Cheat Sheet To Managing Rate Risk Derivative Logic

Http Janroman Dhis Org Stud Ii2008 Caps And Floors Pdf

Difference Between Derivatives Market Finance Investing Investing

Caps Floors And Collars Ppt Download

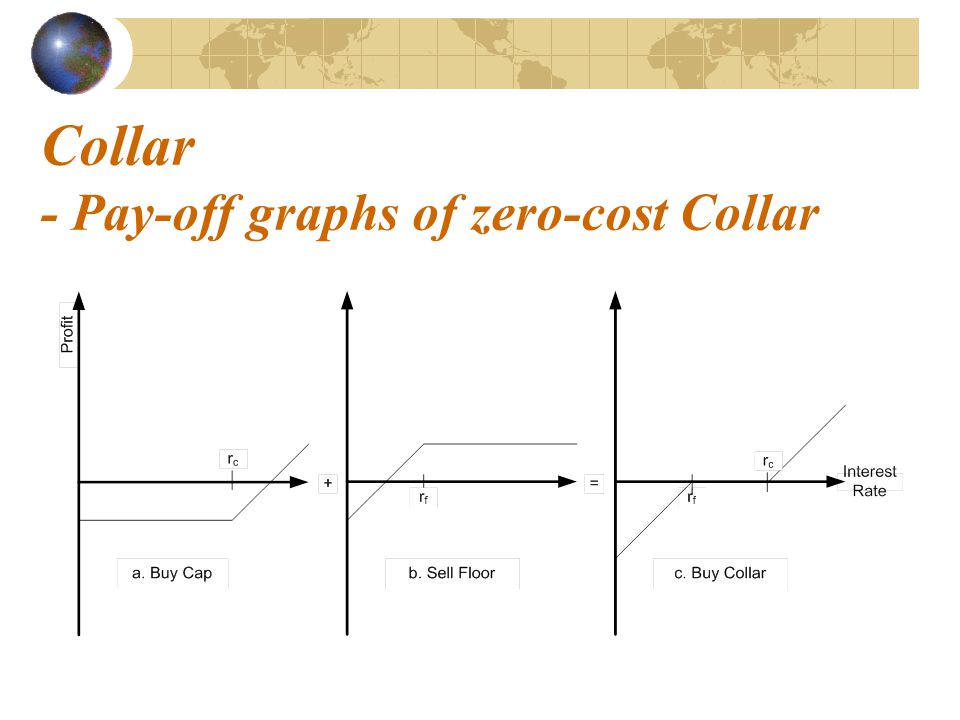

The issuer of a floating rate note might use this to cap the upside of his debt service and pay for the cap with a floor.

Interest rate cap floor and collar.

Interest Rate Caps And Floors Valuation Finpricing

:max_bytes(150000):strip_icc()/strategy-4086857_19201-23485cf7c4bf4dbbb95c93f267285f16.jpg)

Interest Rate Collar Definition

House Plan 3125 00013 Modern Farmhouse Plan 2 556 Square Feet 3 4 Bedrooms 4 Bathrooms Modern Farmhouse Plans Farmhouse Plans House Plans

Multi Period Options Interest Rate Caps Interest Rate Floors Ppt Video Online Download

Options Caps Floors

Cece Marrakesh Lace Ditsy Print Ruffle Cap Sleeve Top Floral Ruffle Top Bohemian Shirts Cap Sleeve Top

Foreign Exchange Markets Quizzes Financial Markets Quiz 24 Questions And Answers Practice Financ Financial Institutions Quiz With Answers Financial Markets

Via Milavdripclub Air Jordan 1 Low Sb Unc In 2020 Sneaker Outfits Women Red Sneakers Outfit Cap Outfits For Women

Http Janroman Dhis Org Finance Bloomberg Capfloorcolar 20explained Pdf

Pin By Joe Mcfarland On Machine Shop Interesting Drawings Blueprints Technical Drawing

I Am A Bride Qipao Cheongsam Collar Design Guide High Collar 2c Mandarin Collar 2c Funnel Collar Lace Collar01 J Cheongsam Fashion Vocabulary Cheongsam Dress

Dog Training A Great Dog Training Tip Is To Make Sure You Understand Other Dogs Are Present When You Puppy Socialization Service Dog Training Puppy Checklist

Rustic Heart Id Name Badge Holder Retractable Reel Bottle Cap Bottle Cap Is Great For Waist Or Lanyard Usage No Al Id Badge Holders Badge Holders Bottle Cap

A Man A Photo And The Search To Find The Person In It Si Com Humans Of New York New York Photos Person

Mississippi State Surgical Cap Surgical Caps Mississippi State Critical Care

Knauf At Timber Expo 2013

Vintage Sweaters 1910s 1920s 1930s Pictures Vintage Sweaters 1910s Fashion Edwardian Fashion

List Of Interest Rate Derivatives Instruments Forex Management

Https Encrypted Tbn0 Gstatic Com Images Q Tbn 3aand9gctxj El7gmhrr0f4kolicj0afo1vur0onjiq7yadlp2cs2mkux5 Usqp Cau

N95 Medical Mask 10 Pcs Ship To Usa Face Maskes Kn95mask In 2020 Medical Masks Medical Mask For Kids

Clean And Green Home Improvements Construction Services Construction Group Real Estate Search

Simingd S11 Smart Bracelet Waterproof Bluetooth Sport Smart Watch Heart Rate Monitor Fitness Smart Bracelet Waterproof Bluetooth Smart Watch Heart Rate Monitor

Cool Via Figtny Love Style Instagood Streetstyle Girl Model Picoftheday Fashion Instalike Blogger Abiti Alla Moda Abbigliamento Vestiti Autunnali

Pin On Cell Phones Accessories

Source : pinterest.com